Every year, tens of thousands of Australians struggle to free themselves from crippling debt. If this is you… Take the first step towards financial relief.

Dealing with debt can feel overwhelming, especially when every option seems confusing or risky. We help you slow things down, understand what each choice really means, and move forward with a plan that fits your situation. We help you understand all your options clearly, without pressure or judgement.

Understand your options clearly

No judgement, just real help

Find a clear path forward

We’re on your side. We guide you through all options and support your decisions.

Debt stress can feel overwhelming, but you do not have to face it alone. Bankruptcy or personal insolvency may be one way to regain control, reduce pressure, and start moving forward. We help you understand your options clearly, check whether bankruptcy is right for you, and support you through the process so you can take the next step with confidence.

Tell us about your situation so we can help you make the right decision for you

We explain ALL your options

(not just bankruptcy)

We are here to guide you every step of the way

Whatever you decide, we work with you to make your journey as easy as possible.

Below are 6 of the most commonly asked questions from people who are considering bankruptcy as a solution to their difficulties.

You can keep a vehicle up to the value of $8,000. (Be sure to ask us to find the “Actual” value of your vehicle. The value is often very different to what you think.)

If your vehicle is worth more than $8,000 and there is no finance on it, you may still be able to keep it by using one of these options

Option 1:

you may be able to speak with your Bankruptcy Trustee (the person who looks after you during your bankruptcy) and ask them if you can pay off the difference over the term of your bankruptcy. Here’s an example. Let’s say that your vehicle is worth $15,000 and you would like to keep it. You could speak with the trustee and let them know that you realise you can only keep a car up to the value of $8,000 but that you would like to keep the car and pay off the difference over the next year or two. Often you will find the Trustee very helpful and accommodating and will be more than happy to work with you on this. (We are also happy to negotiate this for you)

Option 2:

You could simply hand the vehicle to your trustee. He can then arrange for it to be sold and once it is sold your trustee will give you back $8,000 from the sale of the vehicle and pay the rest of the money to your creditors. (People you owed money to.) You can then use this $8,000 to go and buy another vehicle.

What if my vehicle is financed

If your vehicle is under secured finance the situation is quite different. Here are the usual scenarios that exist regarding financed vehicles and Bankruptcy.

Scenario 1:

Often you will find that you owe more on the vehicle than what it is worth. If this is the case and your finance company agree to let you keep the loan, then you can keep the vehicle so long as you continue to pay the loan. (That’s right, you can choose to keep a loan even if you go bankrupt!)

Scenario 2:

If your vehicle is worth up to $8,000 more than you have left on your loan and your finance company agree to let you keep the loan, then you can keep it. For example, if you have a vehicle worth $20,000 and your loan is only $12,000 you can keep the vehicle as you only own $8000 worth of the equity in the vehicle. If you are unsure, ask us.

Scenario 3:

If the vehicle is worth $8,000 or more than the loan, then you will again need to work something out with your Trustee to pay off the difference. (We are happy to negotiate this for you if you want us to.)

Your home is often much more than just a property — it is your safe place, your memories, and your sense of security. It’s completely understandable to worry about what may happen to your house if you are considering Bankruptcy.

The good news is that Bankruptcy does not automatically mean losing your home. Depending on your circumstances, there may be options available to help you keep it. Understanding how Bankruptcy works and getting advice early can make a significant difference, so be sure to involve us in this process.

The first step is to work out how much “Equity” there is in your property.

What is equity?

Equity is the difference between what your property is worth and how much you still owe on it. For example, if your property is worth $500,000 and your mortgage balance is $200,000, then you have $300,000 in equity. This represents the portion of the property that you own.

Whether you own the property yourself or with someone else does not necessarily change the options available to you, however it does change how much equity belongs to you personally. For example, if a property is owned equally by two people and there is $300,000 in equity, then each owner’s share would generally be $150,000.

Once you understand how much equity exists and what portion belongs to you, you can start looking at the possible options.

Option 1:

If you have NO EQUITY in your property, then in many situations the trustee may have no reason to pursue a sale of the property. If your lender is happy for you to continue your mortgage repayments, you may be able to keep your home. In many cases this can be possible provided repayments remain manageable.

Option 2:

If you have a SMALL AMOUNT OF EQUITY in your home (commonly somewhere between $10k and $50k), there may be options available to work with the trustee to retain the property and arrange payment of that equity over time. This amount may then be distributed to creditors. The process can sometimes become complex, but we can help guide you through it.

Option 3:

If you have a LARGER AMOUNT OF EQUITY, the process may require more planning and consideration — however this does not mean you are out of options. Every situation is different. Contact us with the details of your property and circumstances and we can work through the available pathways together and help you understand the best next step.

A lot of people worry that Bankruptcy means they will be banned from travelling overseas. That is not usually the case.

If you are bankrupt and want to travel overseas, you will generally need to complete a form and ask your Trustee for permission before you leave Australia. In many cases, this is a straightforward process. In our experience, clients who are open, cooperative, and up to date with their obligations are usually able to travel.

There are some situations where a trustee may not approve overseas travel. These can include:

Permission is ultimately at the discretion of the trustee.

So yes, overseas travel may still be possible while bankrupt. You simply need to request permission before you go. If you are planning to travel, we can help you understand the process and assist with the application to leave Australia.

One of the most common questions we are asked is “What are the consequences of Bankruptcy?” The honest answer is that there is no one-size-fits-all response because every person’s situation is different.

…and many other factors.

That’s why understanding your own circumstances before making any decision is so important.

That said, there are a few things that commonly apply to many people during Bankruptcy:

Many people are surprised to learn that Bankruptcy does not automatically mean losing everything or putting life completely on hold. Understanding how the rules apply to your specific circumstances can make a significant difference to the outcome.

We recommend completing the FREE Bankruptcy Evaluation so we can help identify any factors that may affect your situation and explain your options clearly. This advice is obligation free and may help you make a more informed decision.

You can become bankrupt in two main ways.

Forced Bankruptcy:

This can happen when a creditor takes legal action through the courts. If a judgment is made against you and the debt remains unpaid, the creditor may apply to have you made bankrupt.

This process can feel stressful and overwhelming. It may involve court documents, legal steps, financial information, and communication with creditors or lawyers. If this has already started, please contact us as early as possible so we can help you understand what is happening and what your options may be.

Voluntary Bankruptcy:

This is when you choose to take control of the situation and apply for Bankruptcy yourself.

While voluntary Bankruptcy can be a more proactive option, the application process can still feel complicated if you are doing it alone. There are forms to complete, documents to gather, and important questions to answer correctly.

To apply for voluntary Bankruptcy, you generally need to:

The good news is that you do not need to manage this process by yourself. We can guide you through each step, help prepare the application properly, and make the process feel much clearer and more manageable.

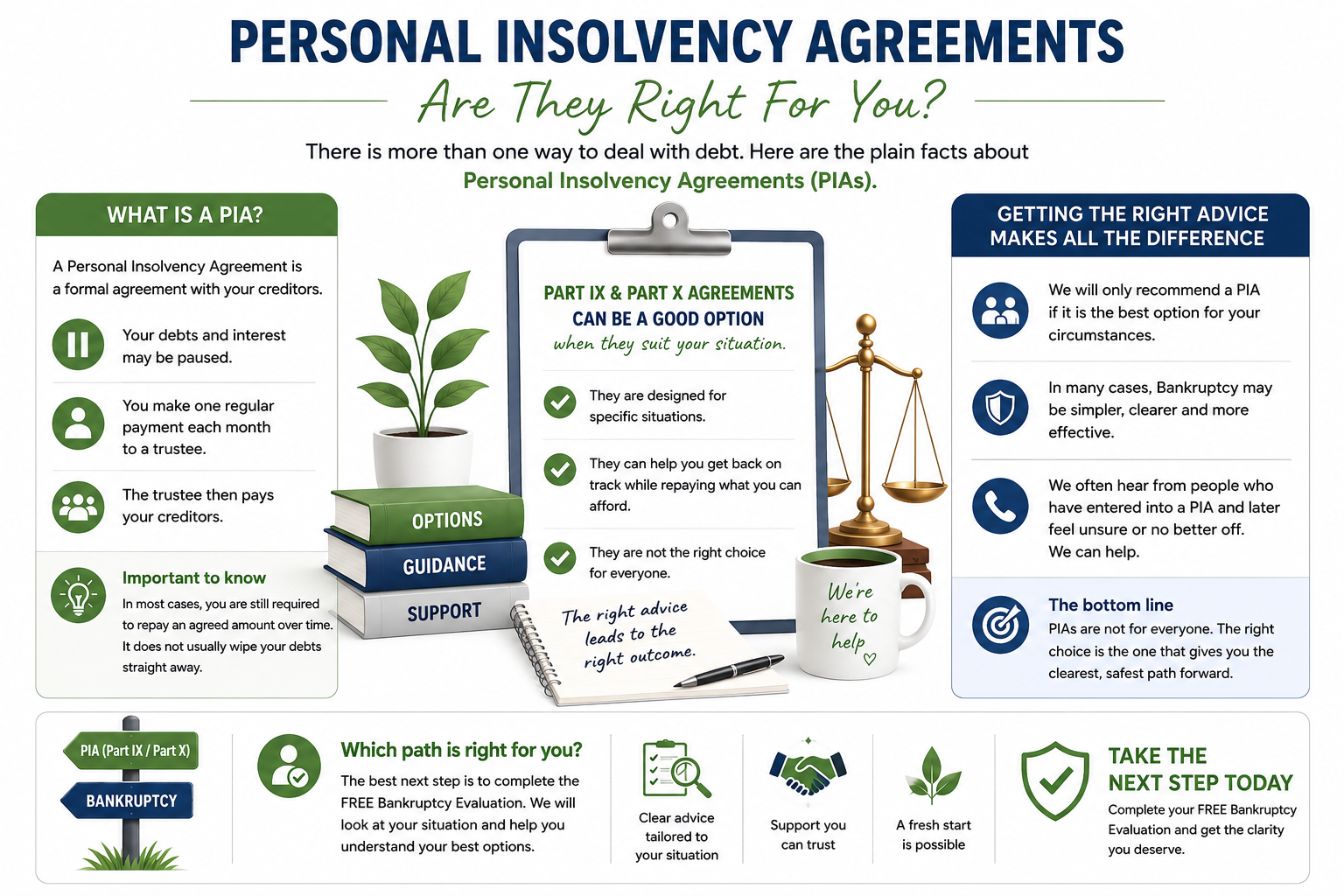

This is a really common question. Many people start looking at their options and quickly realise there is more than one pathway available. One option they may come across is a Personal Insolvency Agreement, often called a PIA.

Personal Insolvency Agreements can include Part IX agreements (Part Nine) and Part X agreements (Part Ten). These are formal debt agreements designed for specific situations.

In simple terms, these agreements may allow your debts and interest to be paused while you make one regular payment to a trustee or administrator. That trustee or administrator then distributes the money to your creditors.

It is important to understand that these agreements do not usually wipe your debts straight away. In most cases, you are still required to repay an agreed amount over time.

For some people, a Part IX or Part X agreement can be a suitable option. For others, it may not provide the fresh start they were hoping for. This is why it is important to get clear advice before making a decision.

We will only recommend a Personal Insolvency Agreement if we genuinely believe it is the best option for your circumstances. In many cases, Bankruptcy may be simpler, clearer, and more effective — but every situation needs to be looked at properly.

We often speak with people who have already entered into a Personal Insolvency Agreement and later feel unsure, frustrated, or no better off. If that has happened to you, please contact us. We can help you understand where you stand and what options may still be available.

So, can these agreements be a good option? Yes, they can be — but only when they properly suit your situation.

The best next step is to complete the FREE Bankruptcy Evaluation. We can then look at your circumstances and help you understand whether a Part IX, Part X, Bankruptcy, or another option is most appropriate for you.

Personal Insolvency Agreements are not for everyone. The right choice is the one that gives you the clearest, safest path forward.

We share information about all of your options, so that you can make informed decisions about your future

Start with a free evaluation and understand your options clearly.

No obligation. No pressure. Just help!